TRICARE For Life and Medicare

TRICARE is health care for active-duty and retired military service members. TRICARE for Life is a supplement to Original Medicare for retired service members. It helps cover additional services and costs related to health care needs, including prescription drugs.

- Written by Stephen Kates, CFP®

Stephen Kates, CFP®

Principal Financial Analyst for RetireGuide.com

Stephen Kates is a Certified Financial Planner™ professional and personal finance expert with over a decade of experience working with individuals and families who need help with their finances. With experience as a financial advisor for two of the largest financial firms in the country, Stephen has worked with hundreds of clients to build comprehensive financial plans to grow and protect their wealth.

Read More- Edited By

Lamia Chowdhury

Lamia Chowdhury

Financial Editor

Lamia Chowdhury is a financial content editor for RetireGuide and has over three years of marketing experience in the finance industry. She has written copy for both digital and print pieces ranging from blogs, radio scripts and search ads to billboards, brochures, mailers and more.

Read More- Reviewed By

Christian Worstell

Christian Worstell

Medicare Expert

Christian Worstell is a licensed health insurance agent and an established writer in the sector, with articles featured in Forbes, MarketWatch, WebMD and more. His work has positively impacted beneficiaries nationwide and empowers them to make strong health care decisions.

Read More- Published: October 19, 2020

- Updated: May 8, 2023

- 8 min read time

- This page features 8 Cited Research Articles

Key Takeaways- TRICARE is the military health insurance coverage for active duty and retired military service members and their families.

- There are many TRICARE plans to fit the needs of the armed service members.

- TRICARE offers enrollees additional coverage beyond Medicare and pays deductibles for Medicare Part B.

- TRICARE acts as a prescription drug plan for all members active or retired.

What Is TRICARE?

TRICARE is the military health insurance system that provides medical coverage for over 10 million active-duty and retired military members and their families. The name TRICARE comes from the three basic plan options that the program began with in the 1990s.

Since then, the options for enrolled members have expanded to suit the various needs of its members. There are now many different options for both health and dental insurance depending on individual users’ circumstances and medical provider preferences.

To be eligible for TRICARE, you must satisfy one of the two requirements:- You are active-duty military, retired military, or active/retired in National guard or reserves.

- You are a family member of someone who satisfies the requirement above. You must be registered before being accepted.

There are certain exceptions for separated service members. To learn more about the specifics of enrollment and who is eligible, please visit https://tricare.mil/Plans/Enroll.

TRICARE can serve as a valuable supplement to your Medicare coverage and anyone eligible for TRICARE should understand how the two programs work together in order to optimize your health care strategy.Is TRICARE Medicare?

TRICARE is not Medicare, but it is health insurance. TRICARE is only meant for military or former military service members and their families. There are strict limitations on who can be eligible to use the TRICARE health program.

One big difference is that TRICARE is not limited to individuals who are 65 or older like Medicare, but some exceptions apply. For those individuals who are eligible for Medicare and already have TRICARE, Medicare will become the primary payer for healthcare and TRICARE will act as the secondary payer for coverage of coinsurance and deductibles.

Who Qualifies for TRICARE?

According to the Defense Health Agency (DHA), there are various people who qualify for TRICARE.

TRICARE members include:- Active-duty service members and their family members

- National Guard and Reserve members and their family members

- Retirees and their family members

- Survivors

- Certain former spouses

TRICARE leverages the resources of the U.S. Government Military Health System, as well as civilian healthcare resources and infrastructure, to provide accessible and reliable care for all military service members and their loved ones.

TRICARE vs. TRICARE Prime

While TRICARE represents the umbrella of different health care plans, services and options available to the uniformed service members, TRICARE Prime is a specific care plan available to both active and retired service members.

Active service members are required to participate in the TRICARE Prime plan as part of their active-duty responsibilities. Each member will have a Primary Care Manager (PCM) who will orchestrate care or provide referrals for care that they cannot provide. In addition, the PCM will accept copayments and be responsible for filing claims.

TRICARE Prime is only available in Prime Service Areas, which are determined by the drive time to a military healthcare facility. If service members live outside of a Prime Service Area, they can select other specialty options for TRICARE Prime, which satisfy living in remote locations or overseas.

While active-duty service members are required to enroll in TRICARE Prime, their families are not. Families and dependents of active-duty military may choose either TRICARE Prime or TRICARE Select. The provider describes the difference between the two plans as follows: “TRICARE Prime offers fewer out-of-pocket costs than TRICARE Select, but less freedom of choice for providers.”

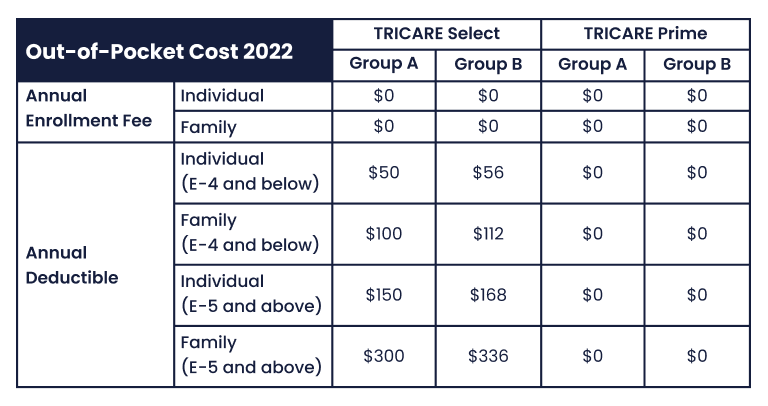

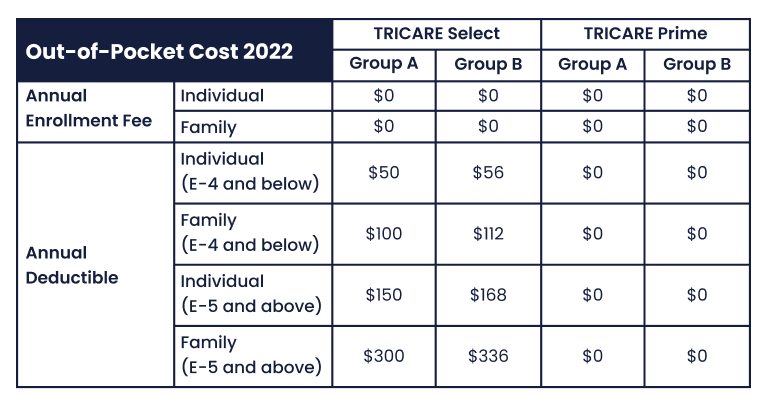

Active-duty service members and their families have no enrollment fees or deductibles. In TRICARE Select, which offers more choice for healthcare providers, there is no enrollment fee, but there is an annual deductible which can range from $50 to $336 depending on status, coverage and service start date. The data in the table below reflect 2022 costs.

Expand

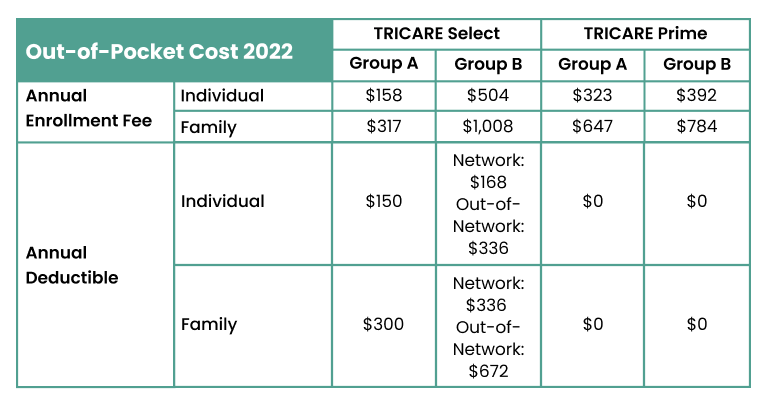

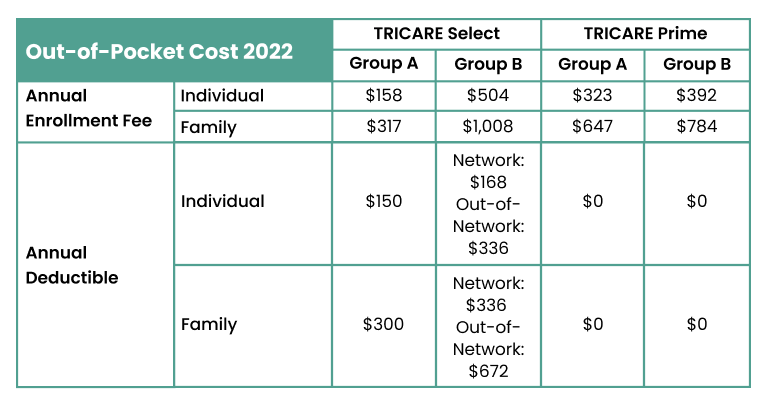

ExpandRetired Military members and their families will be required to pay annual enrollment fees, as well as annual deductibles. The data in the table below reflect 2022 costs.

ExpandSource: TRICARE Newsroom

ExpandSource: TRICARE NewsroomHow Does TRICARE for Life Work with Medicare?

TRICARE for Life (TFL) is a secondary health care plan that supplements Medicare for those who are both TRICARE-eligible and have enrolled in Medicare Part A and B. Unlike other TRICARE plans, TRICARE for Life does not extend coverage to family members or dependents that don’t satisfy these requirements.

Enrolling in TRICARE for Life is not required for active-duty service members like other TRICARE plans, but they are eligible to enroll. For those that do enroll, coverage is available worldwide and begins at the time Medicare Part A and B are in effect.

Through the enrollment in Medicare, all providers who accept Medicare will be accessible. While there are no enrollment fees, enrollees must pay for their own Medicare Part B premiums.

Although many longtime service members think of their TRICARE plan as their main health care coverage, TRICARE for Life will play a secondary role to Medicare. Health care providers will first file claims with Medicare and, if necessary, will then send claims to TRICARE for additional processing.

TRICARE for Life will pay the provider directly for any services that were not covered by Medicare and are TRICARE-covered services.

Out-of-Pocket CostsType of Service Medicare Pays TRICARE Pays You Pay Covered by TRICARE and Medicare Medicare-authorized amount Remaining amount Nothing Covered by Medicare only Medicare-authorized amount Nothing Medicare deductible and cost-share a percentage of the total cost of a covered health care service that you pay. Covered by TRICARE only Nothing TRICARE-allowable amount TRICARE deductible and cost-share Not covered by TRICARE or Medicare Nothing Nothing Billed charges (which may exceed the Medicare or TRICARE-allowable amount) Source: TRICARE PlansTo learn more about service covered, review the TRICARE for Life Cost Matrix.

Is Medicare and TRICARE for Life Enough Coverage?

Between the two programs, most healthcare services are covered by one or both plans. However, there may still be certain procedures that will not be covered, such as cosmetic surgery, acupuncture or eye exams. So, it is important to take an active role in understanding your care and coverage.

In the event your chosen or required care is not covered fully by either plan, it can be beneficial to utilize Medicare Supplement Insurance, also known as Medigap. When traveling overseas, members should be prepared to pay upfront for care or medications and file reimbursement claims.

TRICARE vs. Medigap

Medigap plans are meant to fill in the holes of Original Medicare coverage. Medicare through normal Part A and B cover many health care needs for retirees but can leave some desired or required services uninsured. This is where Medigap plans can be beneficial. Many plans will help pay for costs such as copayments, coinsurance and deductibles.

TRICARE will satisfy many, if not all, the benefits of Medigap plans with exceptions for certain health needs and special circumstances. Through TRICARE for Life, enrollees will have access to the TRICARE prescription drug plan and TRICARE will act as a secondary payer just as most Medigap plans do.

If you are considering what healthcare coverage you need, first speak to your provider who is familiar with your healthcare needs. Review the services covered and not covered by both Medicare and TRICARE to determine whether you will need to fill in any gaps.

TRICARE for Life and Medicare Advantage Plans

Medicare Advantage plans are an alternative way to receive coverage for Medicare Parts A and B. These plans are offered by private health insurance companies that have been approved to offer their Medicare plans to the public.

It is unlikely that using a Medicare Advantage plan will be beneficial when paired with TRICARE for Life for a couple of reasons. The main reason is that TRICARE for Life does not pair as seamlessly with Medicare Advantage in the way Original Medicare does. This may require providers to manually process claims, which can delay billing and other administrative work.

Also, Medicare Advantage plans may not have more to offer than Original Medicare if it’s paired with TRICARE for Life. For example, one of the main reasons people choose Medicare Advantage is for prescription drug coverage, which is already covered in TRICARE for Life.

Before choosing whether to explore a Medicare Advantage plan, consult with your health care provider to explore your options. Depending on the plans available, you may be able to customize features and costs, which could provide additional benefits.

Prescription Drug Coverage with Medicare and TRICARE for Life

TRICARE for Life includes prescription drug coverage as part of its normal health care coverage. It is offered to all beneficiaries at no additional cost.

Routine medication should be ordered and filled through the TRICARE mail-order pharmacy process, whereas other medications for illness, surgery or emergency procedures should be purchased through a local pharmacy or on base. All medications will be billed to Medicare and TRICARE and normal co-pays will apply.

Frequently Asked Questions About TRICARE & Medicare

Do military retirees have to pay for Medicare?Retired military service members will be required to pay for Medicare Part B premiums. While TRICARE for Life does not have any enrollment fees, the cost of Medicare Part B is still paid for by the participant.Does TRICARE for Life pay Medicare Part B deductible?TRICARE for Life will cover Medicare deductibles, as well as the costs of other services not covered by Medicare. Not all services are covered by TRICARE, so it is important to understand what will and won’t be covered through both Medicare and TRICARE.Do you need Medicare if you have TRICARE for Life?Medicare enrollment is recommended for any retirees over the age of 65 or who satisfy the other eligibility requirements for Medicare coverage.Last Modified: May 8, 2023Share This Page Stephen Kates, CFP® Principal Financial Analyst for RetireGuide.comStephen Kates is a CFP® professional with over 15 years of experience helping individuals and families grow and protect their wealth. Stephen is the Principal Financial Analyst for RetireGuide.com where he focuses on providing strategic insights on current market and industry topics such as wealth management, retirement planning, and investing. Stephen has appeared on national broadcasts, including NBC, CBS, and Fox Business, and has contributed to leading digital publications such as CNET, International Business Times, and Newsweek.

Stephen Kates, CFP® Principal Financial Analyst for RetireGuide.comStephen Kates is a CFP® professional with over 15 years of experience helping individuals and families grow and protect their wealth. Stephen is the Principal Financial Analyst for RetireGuide.com where he focuses on providing strategic insights on current market and industry topics such as wealth management, retirement planning, and investing. Stephen has appeared on national broadcasts, including NBC, CBS, and Fox Business, and has contributed to leading digital publications such as CNET, International Business Times, and Newsweek.- Certified Financial Planner™ Professional Since 2013

- Excellence in Action Award Recipient for Client Service

- Bachelor’s in economics from Trinity College in Hartford, CT

Edited By Lamia Chowdhury Financial EditorReviewed By

Lamia Chowdhury Financial EditorReviewed By Christian Worstell Medicare Expert

Christian Worstell Medicare Expert8 Cited Research Articles

- Absher, J. (2022, November 7). TRICARE Prime Coverage Details. Retrieved from https://www.military.com/benefits/tricare/prime/tricare-prime-coverage-details.html

- TRICARE. (2022, September 27). Becoming Medicare Eligible. Retrieved from https://www.tricare.mil/medicare

- TRICARE. (2021, October 4). TRICARE 101. Retrieved from https://www.tricare.mil/Plans/New

- Military Benefit Association. (2021, May). What is TRICARE. Retrieved from https://www.militarybenefit.org/membership-benefits/get-educated/what-is-tricare/

- Ostrom, S. (2020, November 16). What TRICARE For Life Enrollees Should Know About Medicare Advantage Plans. Retrieved from https://www.moaa.org/content/publications-and-media/news-articles/2020-news-articles/what-tricare-for-life-enrollees-should-know-about-medicare-advantage-plans/

- TRICARE. (2018, June 5). Plans. Retrieved from https://www.tricare.mil/Plans/HealthPlans/TFL

- U.S. Department of Health and Human Services. (2014, September 11). Who Is Eligible for Medicare. Retrieved from https://www.hhs.gov/answers/medicare-and-medicaid/who-is-eligible-for-medicare/index.html

- Centers for Mediare and Medicaid Services. (n.d.). Medicare Advantage Plans. Retrieved from https://www.medicare.gov/sign-upchange-plans/types-of-medicare-health-plans/medicare-advantage-plans

- Edited By

Calling this number connects you to one of our trusted partners.

If you're interested in help navigating your options, a representative will provide you with a free, no-obligation consultation.

Our partners are committed to excellent customer service. They can match you with a qualified professional for your unique objectives.

We/Our Partners do not offer every plan available in your area. Any information provided is limited to those plans offered in your area. Please contact Medicare.gov or 1-800-MEDICARE to get information on all of your options.

888-694-0290Your web browser is no longer supported by Microsoft. Update your browser for more security, speed and compatibility.

If you need help pricing and building your medicare plan, call us at 844-572-0696