Long-Term Care Riders for Annuities

Long-term care riders for annuities provide a financial backstop for long-term health care costs. Our guide outlines the specifics of long-term care riders, how they work and the pros and cons of adding one to your annuity contract.

- Written by Thomas Brock, CFA®, CPA

- Edited By

Savannah Pittle

Savannah Pittle

Senior Financial Editor

Savannah Pittle is a professional writer and content editor with over 16 years of professional experience across multiple industries. She has ghostwritten for entrepreneurs and industry leaders and been published in mediums such as The Huffington Post, Southern Living and Interior Appeal Magazine.

Read More- Reviewed By

Brandon Renfro, Ph.D., CFP®, RICP®, EA

Brandon Renfro, Ph.D., CFP®, RICP®, EA

Retirement and Social Security Expert

Brandon Renfro is a Retirement and Social Security Expert and financial planner. He focuses on helping clients create a secure financial future in retirement and co-owns Belonging Wealth Management. He is also a former finance professor and writes for several publications.

Read More- Published: October 3, 2023

- Updated: February 26, 2025

- 7 min read time

- This page features 7 Cited Research Articles

- Reviewed By

- Long-term care riders for annuities supply extra funds for long-term health care expenses, including in-home care and assisted living.

- If you never need long-term care, money from your rider will pass to your beneficiaries after you die.

- You may need to meet certain conditions to activate your rider, such as needing care for a certain number of months.

- Talk to a financial advisor before buying a long-term care rider. An advisor will help you get the best deal, one that could include inflation protection.

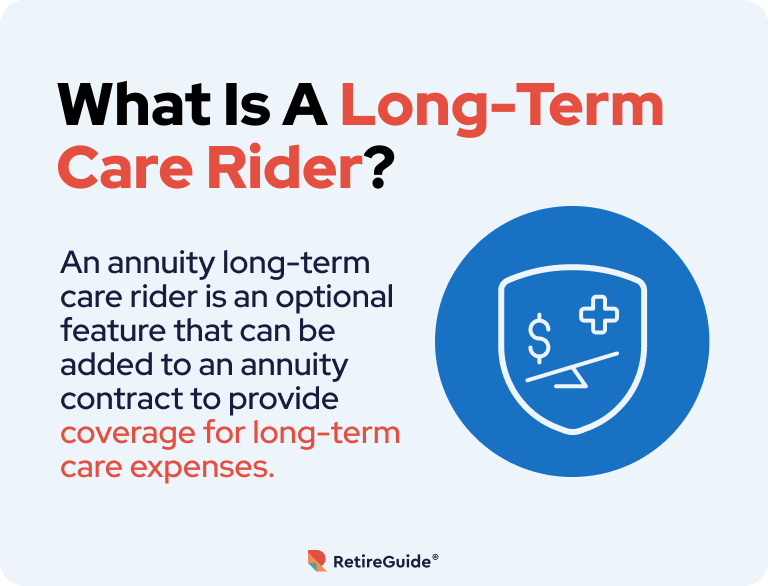

Understanding the Long-Term Care Rider in Annuities

Long-term care riders are insurance to add to your annuity contract, a financial hedge to help you pay for long-term health care. When you add this rider, a part of your premiums gets put into a separate long-term care account. You can withdraw a set amount of money from the account each year to pay for either in-home aid or assisted living residence fees. If you die before using the money, it passes to your beneficiaries.

A long-term care rider can be a good idea if you don’t have any other long-term health insurance.

- You'll pay slightly higher premiums for a rider.

- The benefits from a rider are unlikely to cover all your needs, but a rider with inflation protection is likely to significantly offset any shortfall.

Including a long-term care rider with your annuity is an alternative to purchasing long-term care insurance. It can be more cost-effective than traditional long-term care insurance, but, as with all annuity provisions, it’s very important that you understand what you are buying.

How Do Long-Term Care Riders Work in Annuities?

Long-term care riders separate your product into two parts, the annuity and your long-term care account. Each receives a designated part of your premiums. Just like your annuity funds, your long-term care funds will accrue interest over time, growing steadily until you need the money.

Your annuity provider will disburse some money to you, if you meet certain conditions. In most cases, you must be unable to perform one or more daily activities by yourself, such as bathing and getting dressed, for at least six months. You can use the money you receive to pay for nursing home care or in-home care.

You’ll receive money from your rider until you no longer need it, exhaust the account or surpass the rider’s maximum benefit period. In most cases, the rider’s payouts are not taxed.

Not all types of annuities offer long-term care riders. Those that do may have different conditions for triggering benefits or have other limitations. Consult a financial advisor before buying any kind of annuity or rider, including a long-term care annuity.

How soon are you retiring?

What is your goal for purchasing an annuity?

Select all that apply

Learn About Top Annuity Products & Get a Free Quote

Find out how an annuity can offer you guaranteed monthly income throughout your retirement. Speak with one of our qualified financial professionals today to discover which of our industry-leading annuity products fits into your long-term financial strategy.

For fastest service, call now!

866-219-2282Call NowOr fill out the form

Benefits of Long-Term Care Riders

You may find benefits to adding a long-term care rider to your annuity. Your financial advisor can help you understand how an annuity rider could fit into your retirement plan and whether purchasing one makes sense. The benefits outlined below are the most prominent reasons for doing so.

- Long-Term Care Protection

- If you ever need long-term care, you'll have money to get it.

- Asset Preservation

- Any assets you own can be used for other purposes or left to your heirs instead of being used to fund your care.

- Flexibility in Care Options

- Long-term care rider funds can be put toward any kind of care you need. You can also change your care expenditures without needing approval.

- Comprehensive Coverage

- Long-term care riders cover long-term care for disabilities from illness, accidents and injuries.

- Premium Stability

- Unlike typical long-term care insurance policies, premiums for long-term care annuity riders don't change.

- Potential Tax Advantages

- Payouts from a long-term care rider are usually tax-free.

Drawbacks of Long-Term Care Riders

There are drawbacks to buying a long-term care rider. Discuss them with your financial advisor to confirm whether adding the rider is the right choice for you.

- Increased Cost

- Long-term care riders come with an additional fee.

- Reduced Investment Potential

- Because a long-term care rider diverts some of your premiums from your main annuity fund, buying one may reduce your investment gains.

- Limited Benefit Activation

- You could need temporary long-term care, but not enough to meet the rider’s activation requirements.

- Impact on Death Benefit

- Any long-term care funds you access through your rider will reduce the amount your heirs receive upon your death.

- Policy Limitations and Exclusions

- Some policies restrict how long you can draw your money and limit how you can use it.

- Loss of Control

- Investing money in a long-term care rider restricts how you can invest it.

- Potential Policy Changes

- If your annuity’s terms and conditions change, you may be forced to change your long-term care coverage.

*Ad: Clicking will take you to our partner Annuity.org.

What To Consider When Choosing a Long-Term Care Rider

There’s a lot to consider when deciding which long-term care annuity rider works best for you. Aside from the size of the yearly benefit, you’ll want to consider other factors, such as the annuity provider’s financial stability.

The rider’s terms and conditions are equally important. Read the coverage details and pay special attention to the conditions that activate the benefits — and how long benefits last. Weigh these limitations against the rider’s cost to determine if it offers an acceptable amount of coverage for your budget. Talk to your financial advisor to confirm you’re buying a smart investment.

Understanding the Rate of Inflation

Like any other expense, long-term care expenses are subject to inflation. Without some form of inflation protection, your long-term care rider’s payouts may not pay for enough meaningful care when you need it.

Many long-term care riders address this issue by incorporating automatic compounding benefit increases into their structure. For example, a rider with this type of protection might increase potential payouts by a certain percentage each year. Look for a policy and rider that offers similar benefits. They may cost more than unprotected options, but will ensure your long-term care coverage still is useful over the years.

FAQs About Long-Term Care Riders

- Is a long-term care rider suitable for all types of annuities?

- No. Not all annuities offer long-term care riders. And riders usually come with restrictions and trigger conditions that may make them unsuitable for your needs.

- How will a long-term care rider affect my payouts in the future?

- Purchasing a long-term care rider diverts some of your premiums into a separate fund for long-term care. This means you’ll receive smaller standard payouts from your annuity than you would if you paid the same premiums without the long-term care rider in place.

- Who would benefit the most from having a long-term care rider in their annuity?

- Anyone can benefit from purchasing a long-term care rider for their annuity. However, this coverage is especially beneficial for people with a family history of above-average longevity or disabling illness.

Editor Sierra Campbell contributed to this article.

Connect With a Financial Advisor Instantly

Our free tool can help you find an advisor who serves your needs. Get matched with a financial advisor who fits your unique criteria. Once you’ve been matched, consult for free with no obligation.

- Chartered financial analyst and certified public account

- Managed a $4 billion portfolio for an insurance group

- Master’s degree in finance from Franklin University

7 Cited Research Articles

- Nuss, K. (2023, February 28). Long-Term Care Insurance Via an Annuity Has Many Pros, Some Cons. Retrieved from https://www.medicaleconomics.com/view/long-term-care-insurance-via-an-annuity-has-many-pros-some-cons

- The Journal of the Economics of Aging. (2020, October). Displaced, Disliked and Misunderstood: A Systematic Review of the Reasons for Low Uptake of Long-Term Care Insurance and Life Annuities. Retrieved from https://www.sciencedirect.com/science/article/pii/S2212828X20300013

- National Association of Insurance and Financial Advisors. (2020, June 29). Annuities and LTC Insurance: Two Case Studies in Planning. Retrieved from https://lecp.naifa.org/annuities-and-ltc-insurance-two-case-studies-in-planning

- O’Brien, S. (2019, November 11). These Advisors Help Their Clients Tackle This Unknown Looming Cost. Retrieved from https://www.cnbc.com/2019/11/11/these-advisors-help-their-clients-tackle-this-unknown-looming-cost.html

- Network for Studies on Pensions, Aging and Retirement. (2019, August). A Systematic Review of the Reasons for Low Uptake of Longterm Care Insurance and Life Annuities: Could Integrated Products Counter Them? Retrieved from https://www.netspar.nl/assets/uploads/P20190822_SUR55_Lambregts.pdf

- Tomlinson, J. (2012, December 18). Comparing Long-Term Care Alternatives. Retrieved from https://www.advisorperspectives.com/newsletters12/pdfs/Comparing_Long-Term_Care_Alternatives.pdf

- AARP Public Policy Institute. (2007, May). Can 1 + 1 = 3? A Look at Hybrid Insurance Products with Long-Term Care Insurance. Retrieved from https://citeseerx.ist.psu.edu/document?repid=rep1&type=pdf&doi=e75ade792ddf2c37e0253cb311b285519fd7727f

Calling this number connects you to one of our trusted partners.

If you're interested in help navigating your options, a representative will provide you with a free, no-obligation consultation.

Our partners are committed to excellent customer service. They can match you with a qualified professional for your unique objectives.

We/Our Partners do not offer every plan available in your area. Any information provided is limited to those plans offered in your area. Please contact Medicare.gov or 1-800-MEDICARE to get information on all of your options.

844-897-8632Your web browser is no longer supported by Microsoft. Update your browser for more security, speed and compatibility.

If you need help pricing and building your medicare plan, call us at 844-572-0696