4% Rule for Retirement

The 4% rule is a strategy for making safe withdrawals during retirement while maintaining your savings. The strategy dictates you withdraw 4% of your total savings the first year, then adjust the dollar amount for inflation each following year. This approach should ensure your savings last 30 years. Evaluate your retirement savings to help determine if the 4% rule could help you plan for a financially comfortable future.

- Written by Lindsey Crossmier

Lindsey Crossmier

Financial Writer

Lindsey Crossmier is an accomplished writer with experience working for The Florida Review and Bookstar PR. As a financial writer, she covers Medicare, life insurance and dental insurance topics for RetireGuide. Research-based data drives her work.

Read More- Edited By

Lamia Chowdhury

Lamia Chowdhury

Financial Editor

Lamia Chowdhury is a financial content editor for RetireGuide and has over three years of marketing experience in the finance industry. She has written copy for both digital and print pieces ranging from blogs, radio scripts and search ads to billboards, brochures, mailers and more.

Read More- Published: April 28, 2023

- Updated: December 23, 2024

- 8 min read time

- This page features 4 Cited Research Articles

- Edited By

- The 4% rule is a withdrawal action plan designed to ensure your savings last for about 30 years of retirement.

- In your first year of retirement, you withdraw 4% of your total savings. Every following year, you can withdraw that dollar amount adjusted for inflation.

- The 4% rule is straightforward, easy to apply and has proven reliable through periods of intense economic upheaval.

- You can use other withdrawal strategies in addition to the 4% rule.

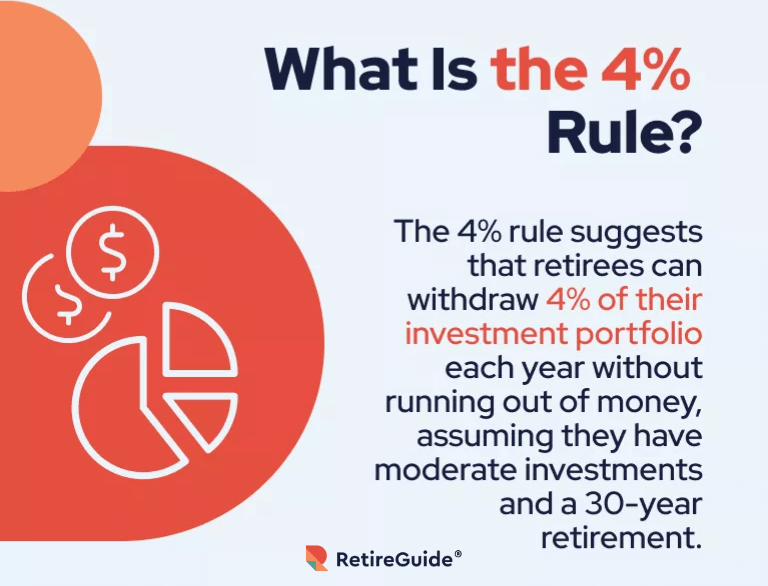

What Is the 4% Rule?

The 4% rule is a general strategy for how much you can safely withdraw from your retirement savings every year while ensuring you don’t diminish your savings too quickly. In your first year of retirement, the 4% rule dictates you withdraw 4% of your savings; in each subsequent year, you can withdraw the same amount adjusted up or down for inflation. As a result, your savings should last 30 years.

Financial advisor, William P. Bengen, first presented the 4% rule in the early 1990s as a guideline for retirees who wanted to plan for a financially comfortable future. After studying historical data on investment returns, he calculated that 4% was the maximum safe withdrawal rate for your first year of retirement — after which the dollar amount (not the percentage) should be adjusted for inflation in each subsequent year.

The practice was rapidly adopted by financial institutions and has helped many people create successful retirement plans. However, it is better to think of 4% as a starting point rather than a strict rule. It’s important to remember the 4% only applies to the very first year of your retirement. After that, you’ll be working with an inflation-adjusted dollar amount.

*Ad: Clicking will take you to our partner Annuity.org.

How Does the 4% Rule Work for Retirement?

The 4% rule is appealing in its simplicity; within the first year of retirement, you can withdraw up to 4% from your retirement savings.

For instance, if you have $2 million saved, the 4% rule suggests you withdraw $80,000 in your first year of retirement. Every year after that, you would withdraw the same amount adjusted for inflation. You can be reasonably assured you’ll be able to live comfortably off your savings for about 30 years.

Following the same example, if inflation was 1% the following year, you would withdraw $80,800 (you would withdraw $81,600 if inflation was 2% or $82,400 if it was 3%). The year after that, you would withdraw $80,800 adjusted again for inflation, and so on through the years.

You might gravitate towards the 4% rule as a withdrawal strategy if you prefer a straightforward approach. While the 4% rule can be a useful starting point when it comes to your retirement planning, it has limitations. As with every withdrawal strategy, there are pros and cons to consider.

- The 4% rule is simple, straightforward and easy to apply, freeing your attention for more enjoyable aspects of your retirement.

- Since the rule always factors inflation into your withdrawal, even in years of high inflation, you won’t have to struggle to make up the difference.

- Bengen’s research covered many financially difficult periods, including the Great Depression, WWII and its aftermath and the soaring inflation of the 1970s. Under those very trying circumstances, the 4% rule was a reliable guide for retirees attempting to make their savings last without sacrificing their standard of living.

- Bengen’s model was built on a perfectly balanced portfolio: 50% stocks and 50% bonds. Modern financial advisors often recommend a 60/40 ratio between stocks and bond investments, as equities tend to outperform fixed-income investments over time.

- The 4% rule doesn’t include the true cost of taxes and/or fees. Instead, it assumes you pay them out of the amount you withdraw.

- Your withdrawal is adjusted for inflation, rather than for how the market performs. In years of high inflation and poor market performance, you might eat into your savings faster than what’s advised.

Inflation

Inflation is the increase in the prices of everyday goods and services. The 4% rule assumes a steady and constant rate of inflation, but unfortunately, inflation doesn’t always work that way.

From 2010 to 2020, the inflation rate was very steady. The average annual inflation rate during that period only once rose as high as 3.16% and also dropped as low as 0.1%. But inflation can also spike suddenly. In 2021, the average inflation rate was 4.7%; in 2022, it grew to 8%. Adjusting for 0.1% inflation does not threaten the security of your savings, but an 8% inflation rate is definitely concerning.

Inflation can also fluctuate from month to month. For instance, in June of 2022, inflation was at 9.1% but by December of that same year, it had dropped down to 6.5%. If you consistently make your withdrawals in the months with the highest inflation rates, you’ll deplete your retirement savings at a faster rate.

Market Conditions

The 4% rule assumes a consistent average rate of return on your investments over time. In reality, the stock market can be volatile. We live in a highly interconnected world. Natural disasters in one country can affect shipping worldwide. Local wars affect trade all around the globe. Markets rise and fall faster today than ever before.

In years of poor market performance, it might be wise to withdraw a smaller amount to prolong the life of your savings. A recent report from Morningstar, an investment research company, suggests that after a year of poor market performance, you might consider reducing your withdrawal amount by 10% so that your total savings don’t shrink too quickly.

Longevity Risk

The 4% rule was created to give people a good rule of thumb on how to make their retirement savings last 30 years. Depending on when and how you retire, however, 30 years’ worth of savings may be insufficient. Life expectancy can vary widely based on factors like your general health, access to medical care and family health history. According to the Centers for Disease Control and Prevention, the average life expectancy for both sexes is 76.4 years. However, female life expectancy is notably higher than males’: 79.3 years to 73.5 respectively.

People often have a tendency to underestimate their potential longevity. Since the trend in life expectancy is generally increasing, you may need to adjust your withdrawal rate to ensure that your savings last throughout your entire retirement.

Fees

Investment fees are the costs charged to use investment products such as stocks or bonds, as well as the expense ratio on funds. Other fees, like withdrawal fees, are the transactional cost for moving money out of your account. Then there are the advisory fees you pay to your financial planners, administrators and even taxes. All these fees impact the size of your remaining savings, which can affect how much you should withdraw at any given time.

If your savings are mostly housed in low-cost vehicles like self-managed EFTs, fees will rarely be a problem. But other types of investment vehicles can come with added costs.

Alternative Strategies for Retirement Withdrawal

You can use alternative retirement withdrawal strategies instead of (or in addition to) the 4% rule. The timing of market returns can play an important part in your decision. For example, if market returns are low in your early retirement years, 4% may be too much to take out; if returns are high, 4% could be more than sufficient. When you decide to take Social Security can also influence how much you need to withdraw from your savings each year.

Depending on your needs and plans, you might find that other withdrawal strategies better suit your situation.

Annuities

Purchasing an annuity is another method you can use to keep from outliving your savings. Annuities are issued by life insurance providers, though they are specifically designed to protect the future of your income, rather than the financial stability of your beneficiaries.

You can use a portion of your savings to purchase an annuity. This would provide you with tax-deferred income, either instead of, or in conjunction with the 4% rule.

*Ad: Clicking will take you to our partner Annuity.org.

Dynamic Withdrawals

The 4% rule is a fixed withdrawal strategy. Although the actual dollar amount of your withdrawal will vary year-to-year, 4% is a single fixed rate. If you see your needs changing from year to year, you might consider adopting a dynamic withdrawal strategy instead.

A dynamic withdrawal strategy means you alter the amount of your withdrawal based on market performance, rather than solely adjusting for inflation. You choose and set guardrails for the percentage to be withdrawn in times of both good and substandard market performance, tailoring your withdrawals based on your own needs and comfort. This strategy requires more attention and in-person handling than the 4% rule.

The Bucket Strategy

With the bucket strategy, you divide your retirement savings into three different buckets. The first bucket consists of cash or no-risk financial vehicles, like Social Security or CDs, for living expenses (three to five years’ worth). The second bucket is for medium-risk holdings, like bonds. The third bucket is for your highest-risk investments, your equities.

With this strategy, you can replenish your first bucket and your living expenses with the income earned from the other two buckets. The exact amount of your savings you put in the two higher-risk buckets is up to you. You can change the allocation as your need and comfort level allows.

Frequently Asked Questions About the 4% Rule

Editor Malori Malone contributed to this article.

Connect With a Financial Advisor Instantly

Our free tool can help you find an advisor who serves your needs. Get matched with a financial advisor who fits your unique criteria. Once you’ve been matched, consult for free with no obligation.

- Special focus on content about life insurance, Social Security, Medicare and certificates of deposits (CDs)

- Research-based data drives her work

- Bachelor’s degree in English from the University of Central Florida

4 Cited Research Articles

- Centers for Disease Control and Prevention. (2023, Feb 7n.d.). Life Expectancy. Retrieved from https://www.cdc.gov/nchs/fastats/life-expectancy.htm

- Benz, C. et al. (2022, December 12). The State of Retirement Income: 2022. Retrieved from https://www.morningstar.com/lp/the-state-of-retirement-income

- Bengen, W.P. (1994, October). Determining Withdrawal Rates Using Historical Data. Retrieved from https://img-cdn.tinkoffjournal.ru/-/bengen1.pdf

- US Inflation Calculator.com. (n.d.). Current US Inflation Rates 2000-2023. Retrieved from https://www.usinflationcalculator.com/inflation/current-inflation-rates

Calling this number connects you to one of our trusted partners.

If you're interested in help navigating your options, a representative will provide you with a free, no-obligation consultation.

Our partners are committed to excellent customer service. They can match you with a qualified professional for your unique objectives.

We/Our Partners do not offer every plan available in your area. Any information provided is limited to those plans offered in your area. Please contact Medicare.gov or 1-800-MEDICARE to get information on all of your options.

844-897-8632Your web browser is no longer supported by Microsoft. Update your browser for more security, speed and compatibility.

If you need help pricing and building your medicare plan, call us at 844-572-0696